Hedge Your Bets

The Current Outlook for Hedge Funds

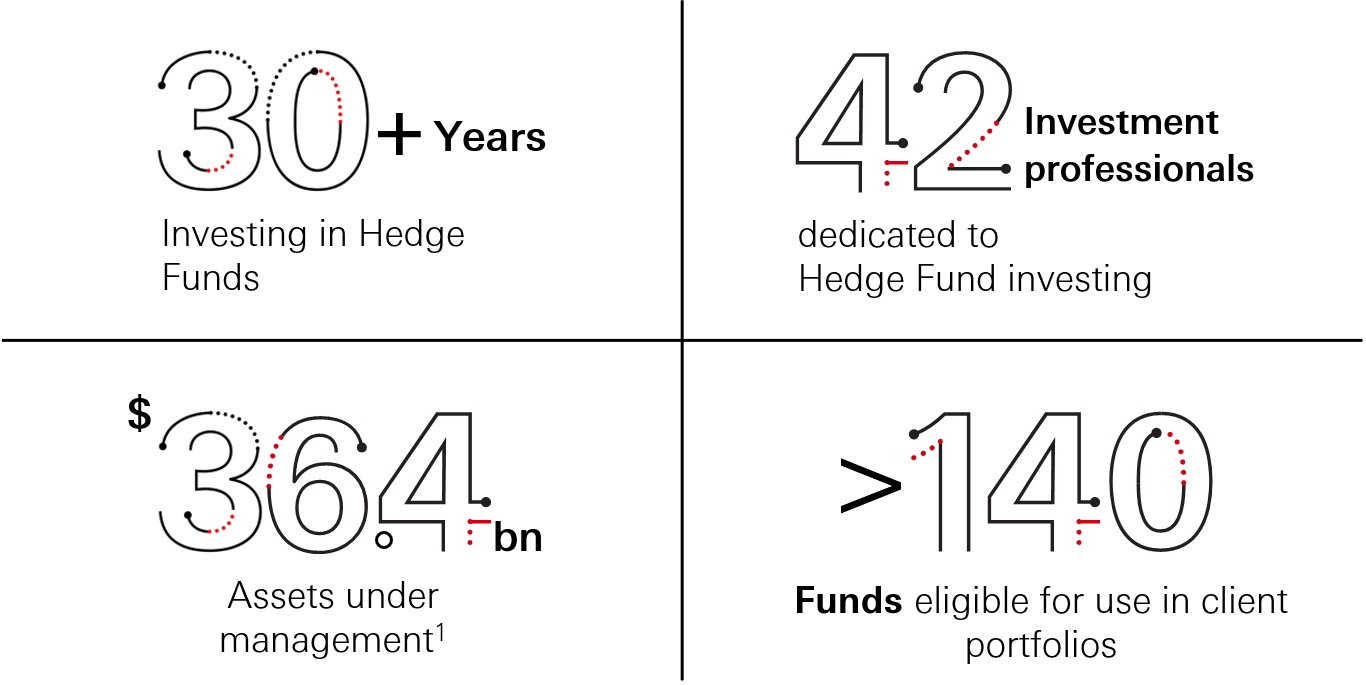

We have spent much of 2026 evidencing to our clients and prospects the benefits of allocating to hedge funds as part of their wider portfolio construct. With a 30+ years’ experience in advising on and investing in hedge fund solutions for our clients, the HSBC hedge fund platform has successfully navigated some of the most turbulent market environments ever witnessed, both in the hedge fund industry but also the wider financial ecosystem in which hedge funds operate. With our three decade track record in mind, we continue to hold a strong conviction in the value hedge funds can play in client portfolios in both the present market environment as well as for years to come.

This paper will explain our rationale for why hedge funds could offer an opportunity at present but also go on to look at some of the long-term trends we are seeing in the hedge fund space, and what this can mean for hedge fund investing moving forward.

The current market environment

We believe there is an abundance of opportunity at present in markets, which hedge funds are well positioned to capitalise on given their ability to invest across different financial instruments.

Macro – A fertile macro trading environment as uncertainty, disruption and volatility persist (especially given the elevated rates and geopolitical picture). In saying that, consistent alpha generation could prove difficult given episodic bouts of volatility, thus emphasising the need for astute manager selection.

Managed Futures – We continue to believe timing trend-following allocations is unlikely to add consistent value, thus the focus is on building resilient and consistent exposure. A blend of both alternative and traditional trend followers offers greater diversification with more idiosyncratic returns.

Equity Long/Short – We would expect managers who harvest rising stock dispersion through disciplined stock selection and thematic positioning while keeping overall market exposure controlled to bear fruit in this market. In Asia, cheaper valuations and uneven liquidity may be supportive of both long and short alpha.

Event Driven and Credit – The strategy is positioned for an active opportunity set, with a preference for multi-discipline managers who can allocate across capital structures and regions as deal activity remains supportive despite rich valuations and global conflict.

Multi-PM – An opportunity dense hedge fund landscape combined with the strong structural advantages of multi-strategy managers could see managers in the space continue delivering returns. Additionally, we view the scale of these managers as a key differentiator, important for both competition and asset raising.

Should you wish to read more on our current outlook for hedge funds at present, please reach out to your HSBC relationship manager to receive a copy of our Quarterly Hedge Fund Strategy Outlook.

The Longer-Term View

Given it is the 30th anniversary of the HSBC hedge fund platform’s flagship product, much of our recent conversations with clients have covered performance across the last 30 years. However, we have also discussed our view on the longer-term direction of the industry. Given the market paradigm in which we find ourselves, and the re-assessment of portfolio allocation which many investors are performing, we have identified three themes which we feel could shape the hedge fund industry’s future.

The potential impact of artificial intelligence

We’re very aware of the seemingly endless excitement surrounding artificial intelligence, not only for its impact on financial markets but also for the ways in which we work. A consistent theme we hear from managers – and a regular topic of conversation when we meet with them – is the potential benefits that artificial intelligence and large language models can bring to hedge funds. While the opportunities appear extensive, several points are repeatedly highlighted. First, given the intense focus on computer science and coding over the last decade or so, the introduction of AI has been a step-change: much of the coding that has been highly sought-after in recent years can now be completed in a fraction of the time. With a sharp reduction in the cost and time required to build software, the development of new models, strategies, and optimisation tools could enable managers to widen their focus. In addition, many managers see significant scope for productivity gains from AI models’ ability to summarise information while performing multiple actions at once. For example, collating and summarising financial information can support investment decision-making. We are already seeing artificial intelligence and LLMs being integrated into investment processes across the industry, with top tier models now table stakes for operating effectively. The sheer quantum of data which hedge funds are privy to (both internally and externally) provides a huge opportunity for further refinement of investment decision making.

Growth of the largest managers

While the 2010s were a period of more muted performance for hedge fund strategies, the decade also saw the growth of the Multi-PM model. As these platforms developed in the early 2020s, we have seen steady outperformance from these managers versus more single-strategy focused funds across market cycles. Why is this? Ultimately, the broad range of strategies, split across pods that dynamically deploy capital, means there is broad coverage of market environments in which allocators are positioned to deliver compelling returns. 2022 was a notable example. As wider equity markets slumped, many multi-strategy hedge funds delivered positive performance, with some net returns in excess of 20%. We believe this dominance will continue. The mature platforms on which these managers operate create environments well-suited for traders to deliver alpha. In addition, their scale enables them to attract superior talent – an imperative in an ever-more competitive industry. Recent large launches highlight some of the barriers to entry that exist at present, which bolsters the case for established multi-PM managers to continue growing in size. This growth could be reflected in a greater number of strategies being launched, as well as higher total assets under management.

Don’t forget the ‘small’ guys

Much of the initial conversations we have with clients can focus on the biggest players in the hedge fund industry. However, as one of the largest hedge fund allocators globally, we continue to see value creation in an array of the relatively smaller managers, both established and new launches. This value creation is evidenced in the number of multi-PM hedge funds which are increasingly allocating to external managers as a way to diversify their own Fund’s returns without having to necessarily build out a given team. In noting the potential benefits of AI for hedge fund managers, we believe there is scope for this to be of particular benefit for smaller managers. Where in a pre-AI era employing first-rate software engineers was imperative to competing as a hedge fund, AI models being able to perform the same role to a very similar degree could somewhat narrow the gap between more junior hedge fund platforms, and those established players with years of experience.

What does this mean for investors?

Taking into account are more short-medium term outlook as well as our more long term outlook, it is clear that the hedge fund industry and hedge funds as an asset class will continue to be a key consideration for many asset allocators when looking to diversify portfolios away from the traditional 60/40 portfolio construct. The prevailing market provides a fertile environment for hedge fund strategies, with the potential long term trends also a tailwind for the continued longevity of the asset class.

With hedge funds back in vogue as the alternative asset of choice, investors should weigh a few key considerations before allocating capital to maximise their chances of achieving attractive risk-adjusted returns.

- Robust Due Diligence – Investors should perform ample and granular due diligence before allocating to a given hedge fund manager. With the potential for material gains in productivity, there is the potential for greater performance dispersion amongst managers who develop and improve at differing rates. Consequently, it is imperative for investors to perform qualitative, quantitative, and operational due diligence to ensure the returns of managers and their processes are relatively strong, and also repeatable

- Access To Managers – With our expectation for the largest managers to grow further with new products and/or wider capital raises, getting access to these managers will be an important driver of returns, especially given their strong track record in delivering returns across market environments

- Diversified Allocations – We believe investors, especially those who are new to allocating to hedge funds, should look to maintain a diversified portfolio of different managers to emphasise the diversification benefits the wider asset class can have for traditional asset allocation. Not all hedge funds are the same, and so allocating to a selection of managers could enhance risk-adjusted returns whilst limiting the downside

The HSBC Hedge Fund Platform has an extensive track record in performing robust due diligence (both investment and operational) on hedge funds to create diversified hedge fund solutions for our clients with allocations to what we view are best-in-class managers – many of whom are hard to access. As a truly global, well-resourced investment team with strong industry connections, we are able to evaluate a significant quantum of managers on a continuous basis to onboard top talent, both established and newly launched.

HSBC Hedge Fund Platform

Past performance does not predict future returns. For illustrative purposes only. The return may increase or decrease as a result of currency fluctuations. Diversification does not ensure a profit or protect against loss. Source: HSBC Asset Management Alternatives, Bloomberg. As at May 2026. 1) AUM figure as of March 2026.

Key Risks

Investors in hedge funds should bear in mind that these products can be highly speculative and may not be suitable for all clients.

The value of investments and any income from them can go down as well as up and investors may not get back the amount originally invested. Past performance does not predict future returns. The return may increase or decrease as a result of currency fluctuations.

There are several key issues that one should consider before making an investment into hedge funds. The risks specific to this type of investment may include, but are not limited to:

Regulation

The hedge fund industry is lightly regulated, with the majority of funds domiciled in offshore jurisdictions. Hedge funds are generally classified as “unregulated” and are not typically subject to the same levels of scrutiny and protection as a traditional investment fund. A thorough due diligence process can mitigate these concerns.Gating

In event that redemptions requests on a particular dealing date are much higher than the normal level and full satisfaction would jeopardise the longer term portfolio balance, a gate or partial execution of redemption requests may be implemented generally on a pro-rata basis.

Side pocket

There may be instances when certain assets in a fund portfolio could become less liquid and the fund manager may segregate these illiquid positions from the main portfolio into a side pocket (or a separate vehicle).

Suspension of redemption

Suspension of redemption is a temporary halt in exiting the fund during a given redemption window. This is a stronger measure than gating because there is no dealing for the fund. This is generally used under special circumstances such as when liquidity conditions have markedly deteriorated in a short period of time or when there are heavy asset outflow such as the loss of a core investor.

Access

Hedge funds operate larger investment minima than traditional investment funds. Investors are often unable to access a hedge fund unless they were willing to invest USD 500,000 to USD2 million.

Liquidity

Hedge funds typically have much longer dealing cycles than traditional investment funds. Depending on the strategy being utilised, a hedge fund may only allow subscriptions and redemptions on a monthly or quarterly basis. Furthermore, some hedge funds have long lock-up periods, where an investor is not permitted to redeem from the hedge fund unless a period of 6 months, a year or even 2 years has passed. Some may allow a redemption before the lock-up period is over, but the investor would have to pay a hefty penalty to be able to do this.

Transparency

Many hedge fund managers are wary of regularly publishing their positions in the belief that this will remove any advantage that they have over their peers. This can pose a problem to the investor, as he or she cannot be certain to which stocks, geographies, markets or even strategies he or she will be exposed to when investing in the hedge fund. However, trusted investors who have built strong relationships with the hedge funds can access this information for the majority of funds, enabling thorough monitoring of the investment.

Manager failure

Over time, a number of hedge funds will close or fail, due to weak performance or operational difficulties. An investor must take this into consideration before making an investment, seeking professional advice to help minimise the risk of investing in a fund that is likely to fail.

Alternatives

There are additional risks associated with specific alternative investments within the portfolios; these investments may be less readily realisable than others and it may therefore be difficult to sell in a timely manner at a reasonable price or to obtain reliable information about their value; there may also be greater potential for significant price movements.

Important Information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark, Spain and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026), through its Italian branch, regulated by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob);

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agency;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D072181_v1.0; Expiry Date: 31.05.2027