Asia credit: Resilience, opportunity and allocation

Asia credit remains resilient with solid investment grade fundamentals and improving high yield conditions, even as returns moderate in line with global credit markets. Amid heightened uncertainty, Asia credit’s compelling opportunities, diversification benefits and risk return profile support a strategic allocation in global portfolios.

Asia USD credit: resilience amid uncertainty

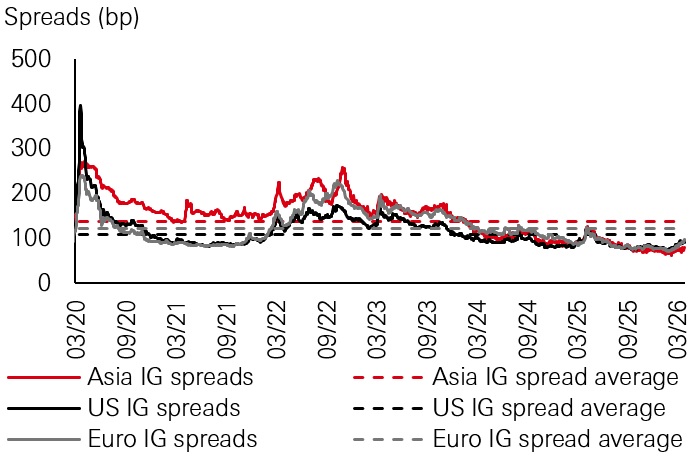

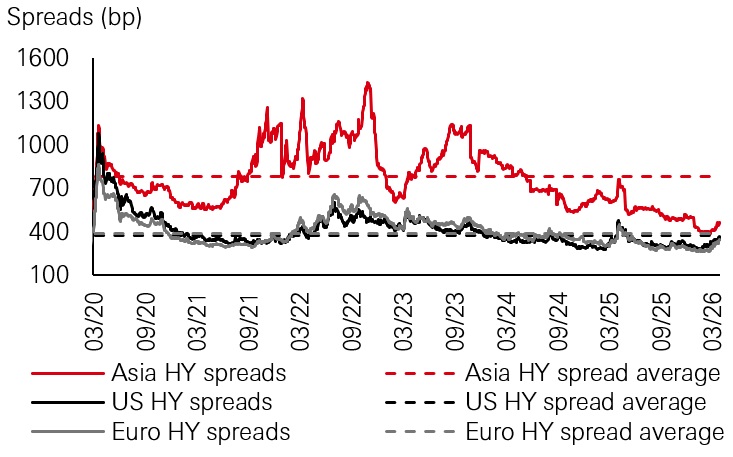

The Asia credit market has demonstrated resilience in recent years despite ongoing global uncertainties: the JPMorgan Asia Credit Index (JACI) posted a 1-year and 3-year return of 5.41 per cent and 19.95 per cent as of 31 March 2026, respectively.1 Spreads in both Asia investment grade (IG) and high yield (HY) markets have tightened over the past five years, with HY making a strong comeback following the property downturn in mainland China, particularly in the last two years (Figures 1 and 2).

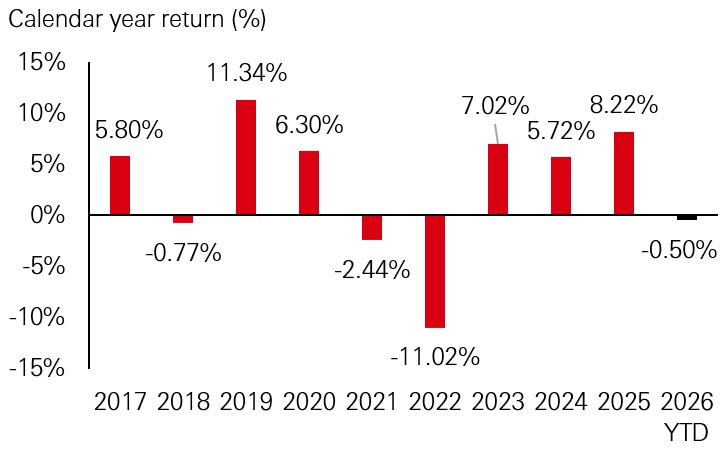

The total return potential in 2026, however, is expected to be more subdued, in line with our global credit views (Figure 3). Asia IG spreads may experience some decompression due to minimal credit premium, but even with moderate widening, spreads are likely to remain tight compared with history (Figure 4). Asia HY offers moderately attractive carry, but valuations across most sectors are also tight historically.

Nevertheless, the Asia credit market is expected to remain resilient in the current market environment. Credit fundamentals remain strong, while technical factors across the region continue to provide a supportive backdrop for the market.

Figure 1: IG credit spreads

Figure 2: HY credit spreads

Note: spread average shown is the 5-year average. Indices used: US IG – ICE BofA US Corporate Index; US HY Corp – ICE BofA US High Yield Index; Asia IG Corp – J.P. Morgan JACI IG Corporate Strip Spread to Worst; Asia HY Corp – J.P. Morgan JACI Non-IG Corporate Strip Spread to Worst; Euro IG – ICE BofA Euro Corporate Index; Euro HY – ICE BofA Euro High Yield Index. Source: Bloomberg; BAML, HSBC Asset Management as of 31 March 2026.

Figure 3: Asia credit returns likely to moderate

Using JACI Index. Source: JP Morgan, HSBC Asset Management, as of 31 March 2026

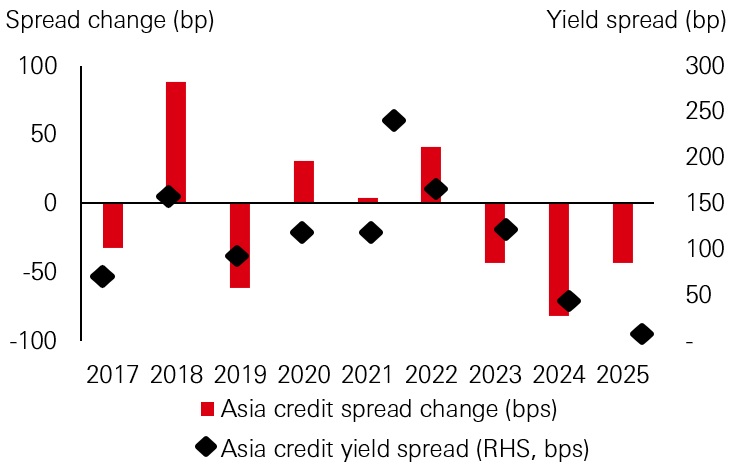

Figure 4: Asia credit spread change vs yield spread

Using JACI Index. Source: JP Morgan, HSBC Asset Management, as of 31 December 2025

Strong fundamentals, diversified universe

Credit fundamentals remain robust in Asia, as reflected in improving leverage and credit metrics and declining default rates.

Among investment grade issuers, net leverage has remained relatively stable, and interest coverage has strengthened (Figures 5 and 6). Credit metrics in Asia IG have broadly evolved as expected, showing stable to gradual improvements from an already strong base. We anticipate moderate fallen angel risks (the risk of an investment grade bond being downgraded to non-investment grade) in 2026, with rising stars (high yield bonds upgraded to investment grade status) primarily concentrated among Indian issuers.

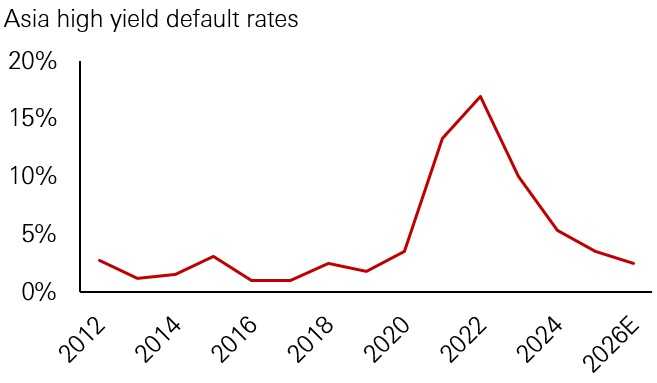

Stress in the Asia high yield market remains largely concentrated in mainland China’s property sector and other idiosyncratic credits. Elevated leverage at the index level is driven primarily by a handful of higher beta names, including in mainland China property, that still carry highly leveraged balance sheets. (Figure 5). Outside of mainland China, underlying credit fundamentals are improving, with default rates on a steady downtrend (Figure 7). Notably, the majority of 2025 defaults have involved previously restructured issuers, while successful refinancing and liability management have helped mitigate broader repayment risk.

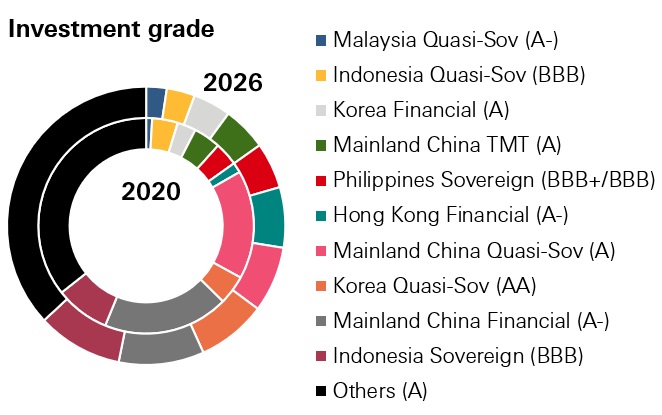

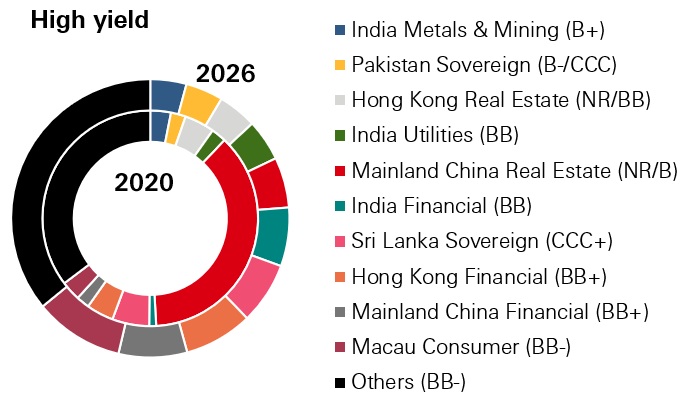

Overall, the JACI Index has maintained broadly stable credit quality of around A-/BBB+, with 84 per cent in investment grade and 16 per cent in non-investment grade.2 Its composition has also become less concentrated, with greater diversification across geographies and sectors (Figure 8). Most notably, the high yield segment has diversified away from mainland China property towards a more balanced sector and geographic mix. Since the property downturn, there has been a sharp decline in mainland China non-investment grade active issuers from 136 in 2020 to 22 in 2026.3 This contraction has meant that the mainland China high yield universe is now concentrated in state-linked bank AT1s, asset management company (AMC) bonds, and outside of financials, a small group of higher-beta names, including mainland China property. Overall, the greater weighting towards non-mainland Chinese sectors, which tend to be less correlated to each other, could help reduce overall market volatility.

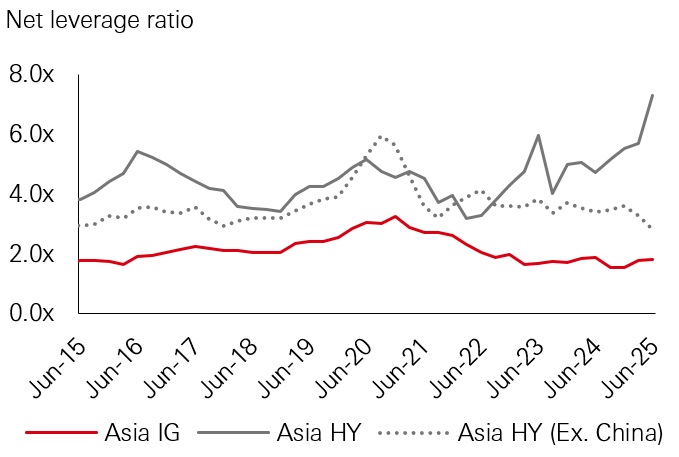

Figure 5: Net leverage: HY ex-China improving, IG relatively stable

Source: BAML, HSBC Asset Management, as of 30 June 2025

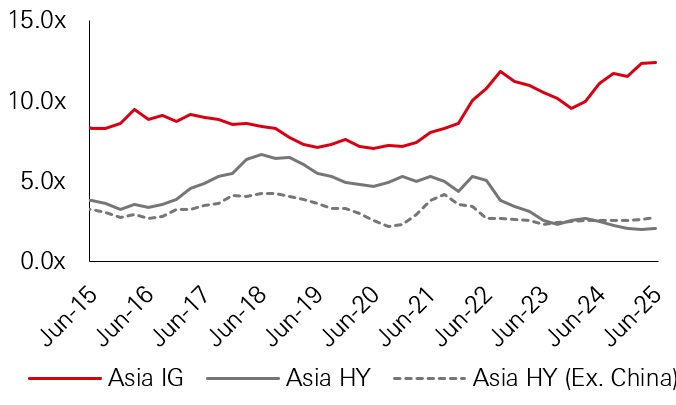

Figure 6: Interest cover: HY stabilised in 1H25 while IG improved

Source: BAML, HSBC Asset Management, as of 31 June 2025

Figure 7: Asia HY default rates trend lower

Source: BAML, HSBC Asset Management, as of 31 December 2025

Figure 8: Asia IG and HY top 10 sector comparison: 2020 (inner rings) vs 2026 (outer rings)

Source: JP Morgan Asia Credit Index, inner rings data are as of 19 January 2020, outer rings data are as of 27 February 2026

2026 technical outlook: rising supply trends

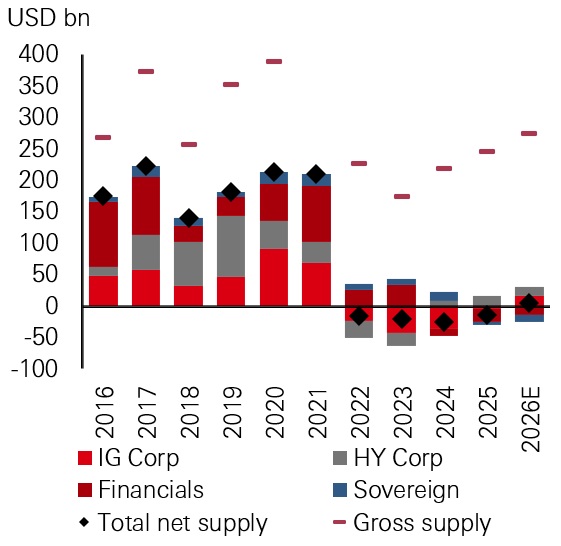

Following years of decline, we anticipate a modest increase in gross supply for 2026. In 2025, gross supply rose 13 per cent year-on-year to USD 247bn in Asia Pacific (including Japan and Australia), and we expect this upward trend to continue (Figure 9). Net supply is expected to reach USD 5.1bn in 2026, equivalent to 0.4 per cent of the JACI Asia Pacific Index. This increase should be balanced by strong demand, supported by ongoing wealth creation and healthy liquidity in the region.

Market supply trends will differ across segments. Mainland China’s supply will likely moderate and Japan’s share should continue to rise. Hong Kong quasi-sovereigns and select sectors, such as technology and renewables, are expected to maintain robust supply due to capex needs. Hong Kong, South Korea, and Thailand are likely to see continued funding requirements in the USD market, given the cost differential between onshore and offshore hedged funding. Generally, we expect the shift in supply towards non-USD credit markets, such as CNH, HKD, AUD, SGD, and EUR, to continue.

Figure 9: Asia-Pacific net supply on uptrend

Source: Bloomberg; BAML, HSBC Asset Management, as of 31 December 2025

Credit investing strategies

In our Asia credit strategies, we are adopting a carry return approach amid an environment of compressed spreads but still attractive all-in yields. Meanwhile, we see select cohorts, such as high yield and unrated credits, as offering potential alpha opportunities. We also maintain diversification across a broader range of fixed income assets, including local currency bonds, emerging market dollar bonds, and convertible bonds, which can be expected to enhance returns. Against this backdrop, strategic country and sector allocation will be key to driving credit performance. We highlight several key investment themes:

AI and technology

We expected AI-related opportunities to be a major investment theme. Select mainland Chinese technology, media, and telecommunications (TMT) names are likely to benefit from wider AI adoption, with higher visibility in direct AI-driven monetisation. Momentum remains strong in Asian hardware tech, such as leading regional foundry and memory chip players, which stand to benefit from data center AI demand and a memory super upcycle. Fundamentals in these segments remain stable, with manageable capex well within financial limits.

Asian technology USD credit now accounts for nearly 10 per cent of the Asia USD investment grade universe, underscoring the rapid growth of tech- and AI-linked exposure.

Opportunities in financials

Asian banks are positioned for a modest fundamental recovery in 2026, driven by improving profitability, stable liquidity, and strengthening capital positions in key markets. We expect to move down the capital structure in search for yield and compelling opportunities and to stay overweight in select Tier 2 and AT1 instruments in Korea, Thailand, Singapore, and Australia.

Elsewhere, select Tier 2 instruments in Asia’s life insurance sector, particularly in Hong Kong, Japan, and Taiwan, offer attractive relative value, despite the sector’s dynamic regulatory environment.

Successful M&A activity is driving improved ratings and growth for Indian private NBFCs, with notable names edging into investment grade due to enhanced capital, better funding access, and strong underwriting. The sector is seeing favourable regulatory changes, easing asset quality pressures, and a shift in the borrowing mix. Despite these longer-term positive trends, Indian private NBFCs remain structurally more sensitive to market conditions. They are predominantly wholesale-funded, inherently pro-cyclical, and – given certain sector concentrations – may face spillover risks when global risk appetite shifts and financial conditions tighten.

Survival bias and technical support in Asia high yield (ex-China property)

Favourable technicals in the USD market is supported by limited supply coming due in 2026, strength underpinned by survival bias as well as robust local funding access across Asia – which makes USD high yield bond issuances less attractive as issuers increasingly shift to cheaper local markets. For instance, in Southeast Asia, corporate credit conditions are benefitting from policy tailwinds and a pick-up in rupiah-denominated corporate bond supply in Indonesia, alongside resilient remittance inflows and constructive local market dynamics in the Philippines. Mainland China high yield “survivors” (mostly in non-property sectors) have also preserved access to domestic refinancing channels. Against this backdrop, we see alpha opportunities that are more idiosyncratic, particularly in mainland Chinese industrials, Indian renewables, and select cyclical sectors that are well-positioned to capitalise on ongoing secular growth trends.

Potential risks

As of this writing and based on our assessment, the initial fundamental impact of a sustained energy price shock on key Asian countries and sectors is expected to be heterogeneous. At the macroeconomic level, sensitivity varies across the region – net oil importers (such as Thailand, the Philippines, and India) feel the pressure given their reliance on energy supply through the Middle East. We believe stress is expected to manifest primarily in local currency and rates markets.

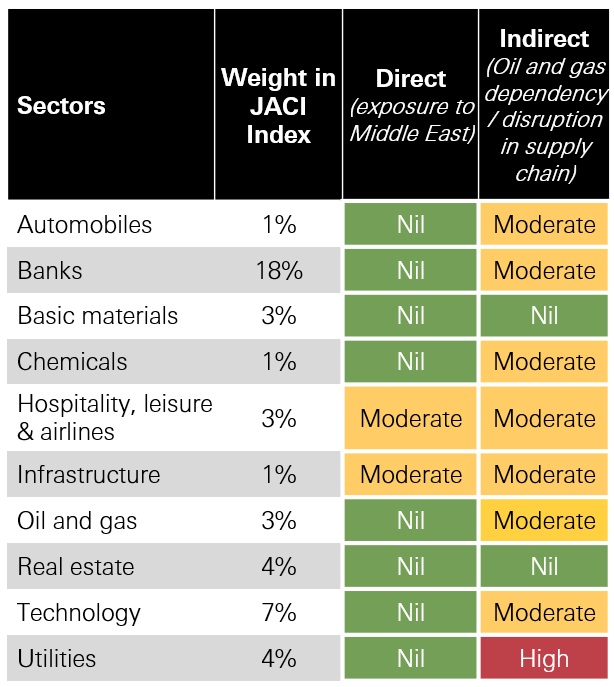

In assessing the implications for Asia USD credit, the market has limited direct credit exposure to the Middle East. A broad sector review further indicates that the potential impact for most sectors – whether through direct Middle East exposure, oil and gas dependency, or supply-chain disruptions – ranges from negligible to moderate (Figure 10).

For Asia credit sectors with greater exposure to energy-price volatility, state ownership and parental support often anchor credit quality and ratings. Even so, within the USD bond universe, the most immediate and identifiable transmission channel of an energy shock is the power utilities sector, where exposure to imported fuel prices and the degree and timing of cost pass-through vary significantly.

Figure 10: Impact assessment of energy price shock on relevant Asia credit sectors

Source: HSBC Asset Management, as of 20 March 2026

These include Korean utilities, given their high sensitivity to volatility in imported fuel prices. In mainland China, gas utilities face higher input costs, but the impact is cushioned by domestic pricing mechanisms and procurement structures. Power generation companies confront higher thermal coal prices, partially offset by a growing renewable mix.

India, Indonesia, and Australia utilities are relatively insulated, as their power generation relies predominantly on domestically sourced coal and natural gas, mitigating direct supply risk. In Japan, power generators may face higher costs due to elevated liquefied natural gas (LNG) and thermal coal prices, compounded by a lag in passing these costs through to end-users. However, the magnitude of the impact will vary by issuer, depending on its generation mix.

Other geopolitical risks continue to linger. Tariff-related uncertainties persist. While Asia credit has demonstrated resilience during periods of external shock, it is crucial to recognise that prolonged uncertainty could have a more pronounced and lasting effect on this asset class.

Meanwhile, the outlook for Asia credit returns is closely linked to US interest rates. However, the US economic landscape remains cloudy. Factors such as job growth, technological disruption from AI, changing productivity trends, and inflation add further complexity, increasing uncertainty for Asia credit returns.

Asia credit spreads also remain sensitive to global risk sentiment. Spreads are currently at multi-year lows, which means there is limited room for error. Any negative shifts in global credit sentiment – whether triggered by developments in the US private credit space, increased AI-infrastructure financing, or concerns about AI-driven industry disruption – may ultimately filter through and exert pressure on Asia credit markets.

Why Asia credit merits a strategic allocation

Asia credit has historically shown resilience during externally driven spread widening episodes, including the COVID-19 pandemic, the 2022 Russia-Ukraine escalation, and “Liberation Day” in 2025. We expect this resilience to continue amid ongoing geopolitical tensions and interest rate uncertainty.

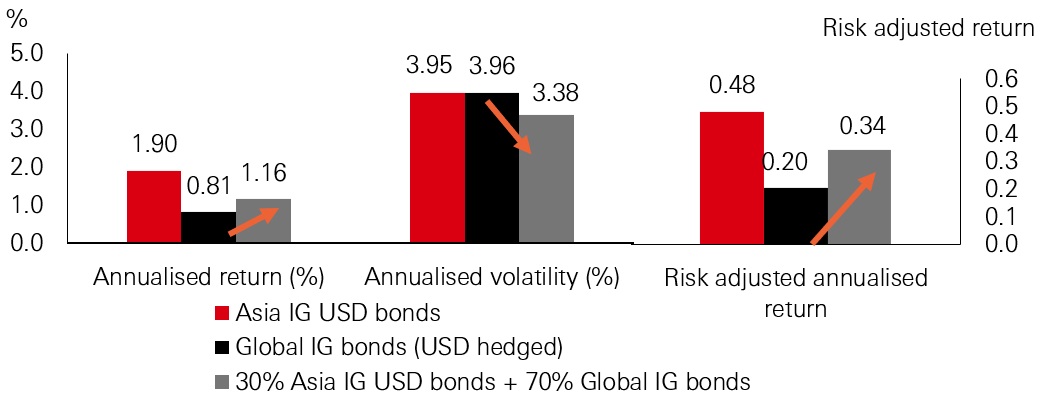

Allocating to Asia IG USD bonds within a broader global IG portfolio can help increase returns and lower overall volatility (Figure 11). Over the last 5-year period, Asia IG credit has meaningfully outperformed global IG bonds, with a 30 per cent allocation adding 35bp in annualised returns. Asia IG credit’s resilience, quality and strong fundamentals support its role in global bond allocations, offering potential diversification benefits, improved portfolio efficiency, and enhanced risk-adjusted returns.

Figure 11: Adding 30 per cent Asia dollar credit to global bond portfolios

(5-year period as of 31 March 2026)

Indices used: Asia IG bonds - JACI Investment Grade Total Return Index, Global IG bonds - Bloomberg Global Aggregate Total Return Index USD hedged. 30 per cent Asia IG USD bonds + 70 per cent Global IG bonds is based on the assumption of no transaction costs and portfolio rebalancing. Past performance does not predict future returns. Hypothetical analysis is for illustrative purpose only and should not be relied on as indication for future result.

Source: HSBC Asset Management, for the past 5 years as of 31 March 2026.

This document provides a high level overview of the recent economic environment. It is for marketing purposes and does not constitute investment research, investment advice nor a recommendation to any reader of this content to buy or sell investments. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination.

Source: HSBC Asset Management, as of April 2026.

Note 1: Source is Bloomberg, using JP Morgan JACI Composite Total Return Index, as of 31 March 2026

Note 2: Source is JP Morgan, as of 13 April 2026

Note 3: Source is JP Morgan, 2020 figure is as of 29 January 2020, while 2026 figure is as of 27 February 2026

Past performance does not predict future returns. Any forecast, projection or target contained in this presentation is for information purposes only and is not guaranteed in any way. HSBC Asset Management accepts no liability for any failure to meet such forecasts, projections or targets. The views expressed above were held at the time of preparation and are subject to change without notice. The information provided does not constitute any investment recommendation or advice. Diversification does not ensure a profit or protect against loss. For illustrative purposes only.

Important information

For Professional Clients and intermediaries within countries and territories set out below; and for Institutional Investors and Financial Advisors in the US. This document should not be distributed to or relied upon by Retail clients/investors.

The value of investments and the income from them can go down as well as up and investors may not get back the amount originally invested. The performance figures contained in this document relate to past performance, which should not be seen as an indication of future returns. Future returns will depend, inter alia, on market conditions, investment manager’s skill, risk level and fees. Where overseas investments are held the rate of currency exchange may cause the value of such investments to go down as well as up. Investments in emerging markets are by their nature higher risk and potentially more volatile than those inherent in some established markets. Economies in emerging markets generally are heavily dependent upon international trade and, accordingly, have been and may continue to be affected adversely by trade barriers, exchange controls, managed adjustments in relative currency values and other protectionist measures imposed or negotiated by the countries and territories with which they trade. These economies also have been and may continue to be affected adversely by economic conditions in the countries and territories in which they trade.

The contents of this document may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose. All non-authorised reproduction or use of this document will be the responsibility of the user and may lead to legal proceedings. The material contained in this document is for general information purposes only and does not constitute advice or a recommendation to buy or sell investments. Some of the statements contained in this document may be considered forward looking statements which provide current expectations or forecasts of future events. Such forward looking statements are not guarantees of future performance or events and involve risks and uncertainties. Actual results may differ materially from those described in such forward-looking statements as a result of various factors. We do not undertake any obligation to update the forward-looking statements contained herein, or to update the reasons why actual results could differ from those projected in the forward-looking statements. This document has no contractual value and is not by any means intended as a solicitation, nor a recommendation for the purchase or sale of any financial instrument in any jurisdiction in which such an offer is not lawful. The views and opinions expressed herein are those of HSBC Asset Management at the time of preparation and are subject to change at any time. These views may not necessarily indicate current portfolios' composition. Individual portfolios managed by HSBC Asset Management primarily reflect individual clients' objectives, risk preferences, time horizon, and market liquidity. Foreign and emerging markets: investments in foreign markets involve risks such as currency rate fluctuations, potential differences in accounting and taxation policies, as well as possible political, economic, and market risks. These risks are heightened for investments in emerging markets which are also subject to greater illiquidity and volatility than developed foreign markets. This commentary is for information purposes only. It is a marketing communication and does not constitute investment advice or a recommendation to any reader of this content to buy or sell investments nor should it be regarded as investment research. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of its dissemination. This document is not contractually binding nor are we required to provide this to you by any legislative provision.

All data from HSBC Asset Management unless otherwise specified. Any third-party information has been obtained from sources we believe to be reliable, but which we have not independently verified.

HSBC Asset Management is the brand name for the asset management business of HSBC Group, which includes the investment activities that may be provided through our local regulated entities. HSBC Asset Management is a group of companies in many countries and territories throughout the world that are engaged in investment advisory and fund management activities, which are ultimately owned by HSBC Holdings Plc. (HSBC Group).

- In Australia, this document is issued by HSBC Bank Australia Limited ABN 48 006 434 162, AFSL 232595, for HSBC Global Asset Management (Hong Kong) Limited ARBN 132 834 149 and HSBC Global Asset Management (UK) Limited ARBN 633 929 718. This document is for institutional investors only and is not available for distribution to retail clients (as defined under the Corporations Act). HSBC Global Asset Management (Hong Kong) Limited and HSBC Global Asset Management (UK) Limited are exempt from the requirement to hold an Australian financial services license under the Corporations Act in respect of the financial services they provide. HSBC Global Asset Management (Hong Kong) Limited is regulated by the Securities and Futures Commission of Hong Kong under the Hong Kong laws, which differ from Australian laws. HSBC Global Asset Management (UK) Limited is regulated by the Financial Conduct Authority of the United Kingdom and, for the avoidance of doubt, includes the Financial Services Authority of the United Kingdom as it was previously known before 1 April 2013, under the laws of the United Kingdom, which differ from Australian laws;

- In Bermuda, this document is issued by HSBC Global Asset Management (Bermuda) Limited, of 37 Front Street, Hamilton, Bermuda which is licensed to conduct investment business by the Bermuda Monetary Authority;

- In France, Belgium, Netherlands, Luxembourg, Portugal, Greece, Finland, Norway, Denmark and Sweden this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026);

- In Germany, this document is issued by HSBC Global Asset Management (Deutschland) GmbH which is regulated by BaFin (German clients) respective by the Austrian Financial Market Supervision FMA (Austrian clients);

- In Hong Kong, this document is issued by HSBC Global Asset Management (Hong Kong) Limited, which is regulated by the Securities and Futures Commission. This content has not been reviewed by the Securities and Futures Commission;

- In India, this document is issued by HSBC Asset Management (India) Pvt Ltd. which is regulated by the Securities and Exchange Board of India;

- In Italy and Spain, this document is issued by HSBC Global Asset Management (France), a Portfolio Management Company authorised by the French regulatory authority AMF (no. GP99026) and through the Italian and Spanish branches of HSBC Global Asset Management (France), regulated respectively by Banca d’Italia and Commissione Nazionale per le Società e la Borsa (Consob) in Italy, and the Comisión Nacional del Mercado de Valores (CNMV) in Spain;

- In Japan, this document is issued by HSBC Asset Management (Japan) Ltd (JRN 3010001124868), regulated by the Financial Services Agengy;

- In Malta, this document is issued by HSBC Global Asset Management (Malta) Limited which is regulated and licensed to conduct Investment Services by the Malta Financial Services Authority under the Investment Services Act;

- In Mexico, this document is issued by HSBC Global Asset Management (Mexico), SA de CV, Sociedad Operadora de Fondos de Inversión, Grupo Financiero HSBC which is regulated by Comisión Nacional Bancaria y de Valores;

- In the United Arab Emirates, this document is issued by HSBC Investment Funds (Luxembourg) S.A. – Dubai Branch (Level 20, HSBC Tower, PO Box 66, Downtown Dubai, United Arab Emirates) regulated by the Capital Market Authority (CMA) in the UAE to conduct investment fund management, portfolios management, fund administration activities (CMA Category 2 license No.20200000336) and promotion activities (CMA Category 5 license No.20200000327).

- In the United Arab Emirates, this document is issued by HSBC Global Asset Management MENA, a unit within HSBC Bank Middle East Limited, U.A.E Branch, PO Box 66 Dubai, UAE, regulated by the Central Bank of the U.A.E. and the Capital Market Authority in the UAE under CMA license number 602004 for the purpose of this promotion and lead regulated by the Dubai Financial Services Authority. HSBC Bank Middle East Limited is a member of the HSBC Group and HSBC Global Asset Management MENA are marketing the relevant product only in a sub-distributing capacity on a principal-to-principal basis. HSBC Global Asset Management MENA may not be licensed under the laws of the recipient’s country of residence and therefore may not be subject to supervision of the local regulator in the recipient’s country of residence. One of more of the products and services of the manufacturer may not have been approved by or registered with the local regulator and the assets may be booked outside of the recipient’s country of residence.

- In Singapore, this document is issued by HSBC Global Asset Management (Singapore) Limited, which is regulated by the Monetary Authority of Singapore. The content in the document/video has not been reviewed by the Monetary Authority of Singapore;

- In Switzerland, this document is issued by HSBC Global Asset Management (Switzerland) AG. This document is intended for professional investor use only. For opting in and opting out according to FinSA, please refer to our website; if you wish to change your client categorization, please inform us. HSBC Global Asset Management (Switzerland) AG having its registered office at Gartenstrasse 26, PO Box, CH-8002 Zurich has a licence as an asset manager of collective investment schemes and as a representative of foreign collective investment schemes. Disputes regarding legal claims between the Client and HSBC Global Asset Management (Switzerland) AG can be settled by an ombudsman in mediation proceedings. HSBC Global Asset Management (Switzerland) AG is affiliated to the ombudsman FINOS having its registered address at Talstrasse 20, 8001 Zurich. There are general risks associated with financial instruments, please refer to the Swiss Banking Association (“SBA”) Brochure “Risks Involved in Trading in Financial Instruments”;

- In Taiwan, this document is issued by HSBC Global Asset Management (Taiwan) Limited which is regulated by the Financial Supervisory Commission R.O.C. (Taiwan);

- In Turkiye, this document is issued by HSBC Asset Management A.S. Turkiye (AMTU) which is regulated by Capital Markets Board of Turkiye. Any information here is not intended to distribute in any jurisdiction where AMTU does not have a right to. Any views here should not be perceived as investment advice, product/service offer and/or promise of income. Information given here might not be suitable for all investors and investors should be giving their own independent decisions. The investment information, comments and advice given herein are not part of investment advice activity. Investment advice services are provided by authorized institutions to persons and entities privately by considering their risk and return preferences, whereas the comments and advice included herein are of a general nature. Therefore, they may not fit your financial situation and risk and return preferences. For this reason, making an investment decision only by relying on the information given herein may not give rise to results that fit your expectations.

- In the UK, this document is issued by HSBC Global Asset Management (UK) Limited, which is authorised and regulated by the Financial Conduct Authority;

- In the US, this document is issued by HSBC Securities (USA) Inc., an HSBC broker dealer registered in the US with the Securities and Exchange Commission under the Securities Exchange Act of 1934. HSBC Securities (USA) Inc. is also a member of NYSE/FINRA/SIPC. HSBC Securities (USA) Inc. is not authorized by or registered with any other non-US regulatory authority. The contents of this document are confidential and may not be reproduced or further distributed to any person or entity, whether in whole or in part, for any purpose without prior written permission.

- In Chile, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Chilean inspections or regulations and are not covered by warranty of the Chilean state. Obtain information about the state guarantee to deposits at your bank or on www.cmfchile.cl;

- In Colombia, HSBC Bank USA NA has an authorized representative by the Superintendencia Financiera de Colombia (SFC) whereby its activities conform to the General Legal Financial System. SFC has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Colombia and is not for public distribution;

- In Costa Rica, the Fund and any other products or services referenced in this document are not registered with the Superintendencia General de Valores (“SUGEVAL”) and no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document is directed at and intended for institutional investors only.

- In Peru, HSBC Bank USA NA has an authorized representative by the Superintendencia de Banca y Seguros in Perú whereby its activities conform to the General Legal Financial System - Law No. 26702. Funds have not been registered before the Superintendencia del Mercado de Valores (SMV) and are being placed by means of a private offer. SMV has not reviewed the information provided to the investor. This document is for the exclusive use of institutional investors in Perú and is not for public distribution;

- In Uruguay, operations by HSBC's headquarters or other offices of this bank located abroad are not subject to Uruguayan inspections or regulations and are not covered by warranty of the Uruguayan state. Further information may be obtained about the state guarantee to deposits at your bank or on www.bcu.gub.uy.

Copyright © HSBC Global Asset Management Limited 2026. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of HSBC Asset Management.

Content ID: D069520_v2.0; Expiry Date: 30.04.2027